*APRs are Annual Percentage Rates and represent the lowest rate possible for each product. APYs are Annual Percentage Yields and represent the highest possible rate for each product. Terms and conditions apply. Rates are subject to change without notice. Click individual rates above for full details and disclosures.

A full-service suite of products and local decisions mean you can expect transparency with your money, putting you in control of your finances.

We strive every day to make it easy for you to do business with us. It’s our mission and our focus. Our founding members formed the credit union for the benefit of their community, as well as for all future generations of members. That’s why when you join GFCU, you’re not just a transaction – you are a part owner and contributor of our financial institution. We believe in people helping people where it matters the most – right here at home.

Services

Manage your money easily? Check.

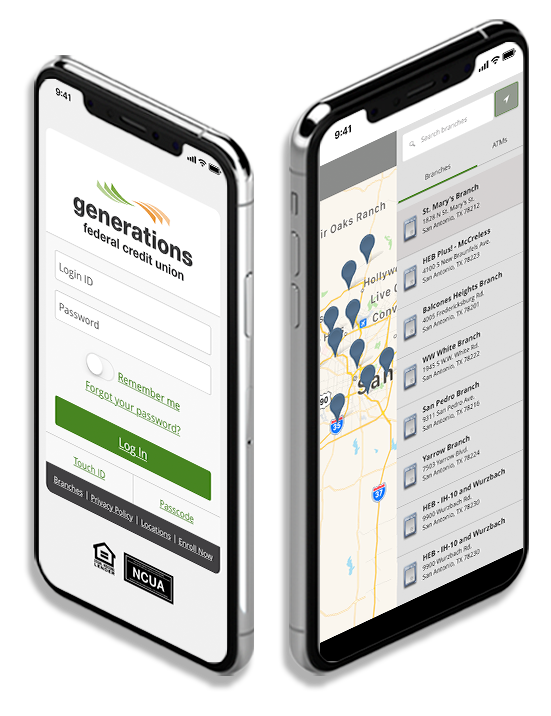

Whether you’re on the go or in the comfort of your home, you can access your accounts quickly and conveniently with our online banking platform, mobile banking app, extensive ATM network and shared branch locations. Plus, with access to additional membership perks like GreenPath and Generations Academy, you have even more resources to help you build a strong financial future.

Additional ServicesWith Online and Mobile Banking, you’re able to manage your accounts from any of your devices, any time of day.

Learn more about E-ServicesWe’re part of the CO-OP ATM Network, giving our members access to nearly 30,000 surcharge-free ATMs nationwide.

Learn more about ATM BankingMake transactions, loan payments and more at any shared branch location while you’re out of town or traveling.

Learn more about Shared BranchingWe’ve partnered with GreenPath, Inc. to bring you even more financial education and counseling resources.

Learn more about GreenPath Financial WellnessWe were built by the hard-working people in our community, and staying true to our roots is one of our highest priorities. We give back through partnerships with local organizations, charity work and staff volunteer events.